All Categories

Featured

Table of Contents

For many people, the most significant issue with the infinite financial idea is that initial hit to very early liquidity caused by the costs. Although this disadvantage of infinite financial can be decreased considerably with correct policy design, the first years will always be the worst years with any kind of Whole Life policy.

That claimed, there are specific unlimited banking life insurance policy plans designed mostly for high very early cash worth (HECV) of over 90% in the initial year. However, the long-term performance will commonly significantly delay the best-performing Infinite Financial life insurance policy plans. Having accessibility to that added 4 figures in the first couple of years may come at the cost of 6-figures later on.

You actually get some significant long-term advantages that assist you recoup these very early prices and after that some. We discover that this hindered very early liquidity issue with limitless banking is extra mental than anything else when extensively discovered. If they absolutely needed every cent of the cash missing from their infinite banking life insurance plan in the very first few years.

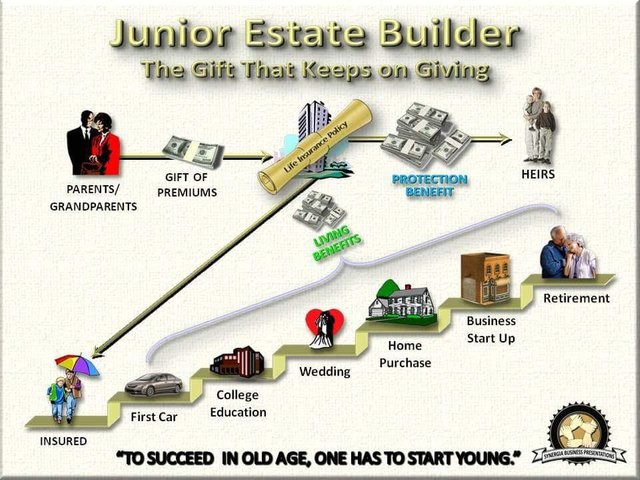

Tag: limitless banking principle In this episode, I talk concerning financial resources with Mary Jo Irmen who shows the Infinite Banking Concept. This topic may be questionable, however I want to get varied views on the program and learn more about various strategies for ranch monetary management. A few of you might agree and others will not, but Mary Jo brings a truly... With the rise of TikTok as an information-sharing system, monetary recommendations and techniques have discovered an unique means of dispersing. One such approach that has been making the rounds is the boundless banking principle, or IBC for short, amassing recommendations from celebs like rap artist Waka Flocka Fire. Nevertheless, while the approach is currently popular, its origins map back to the 1980s when financial expert Nelson Nash presented it to the globe.

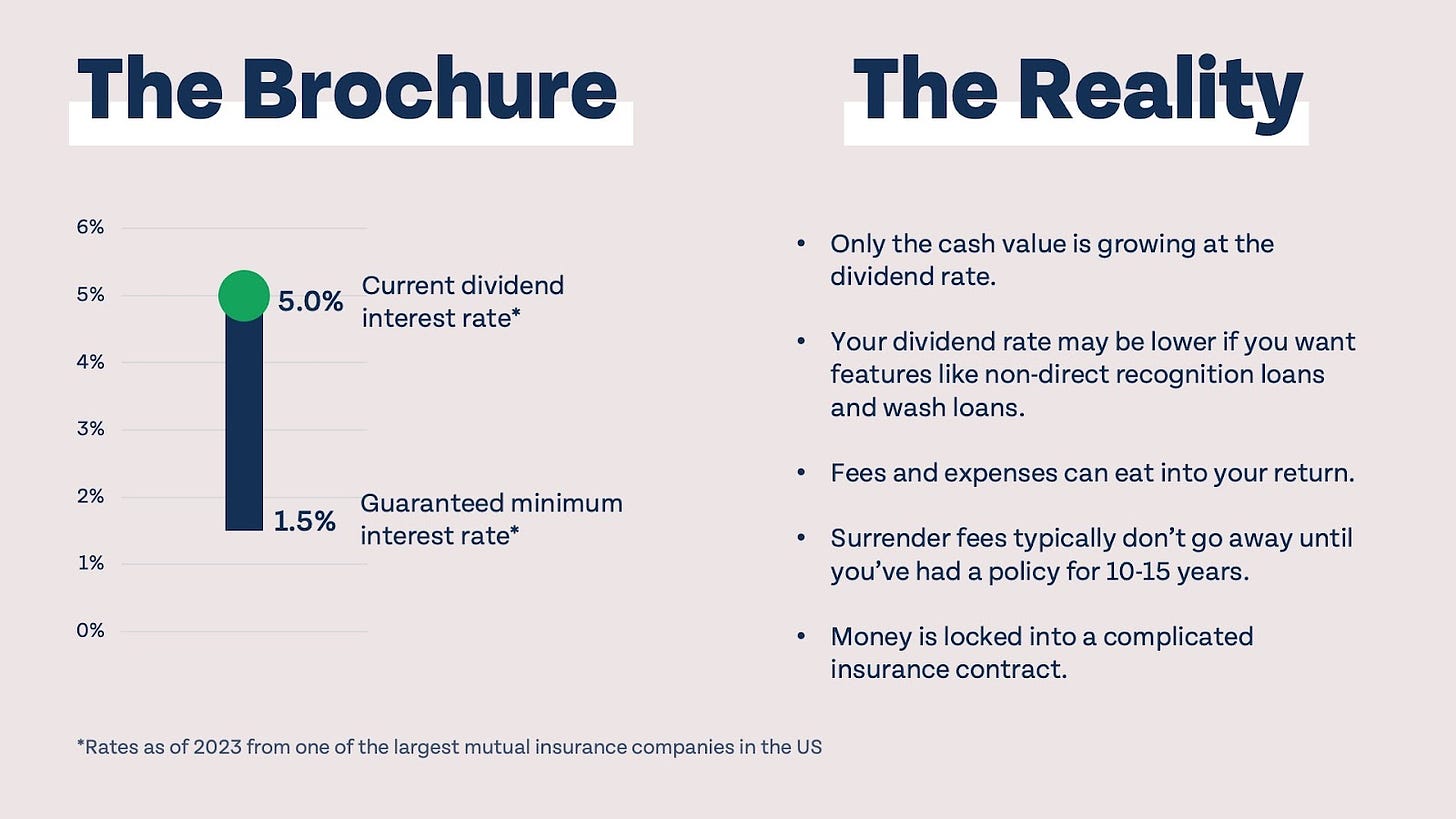

Within these plans, the cash worth grows based on a rate set by the insurer. When a considerable money value gathers, policyholders can obtain a money value lending. These loans differ from conventional ones, with life insurance policy acting as collateral, meaning one could lose their protection if loaning exceedingly without adequate cash worth to sustain the insurance policy expenses.

And while the allure of these policies is evident, there are natural limitations and threats, requiring thorough cash value tracking. The approach's legitimacy isn't black and white. For high-net-worth people or entrepreneur, specifically those utilizing approaches like company-owned life insurance coverage (COLI), the advantages of tax breaks and substance development might be appealing.

Review Bank On Yourself

The allure of infinite financial doesn't negate its obstacles: Price: The foundational demand, an irreversible life insurance policy, is costlier than its term counterparts. Qualification: Not everyone receives entire life insurance policy because of extensive underwriting processes that can leave out those with certain wellness or way of living problems. Intricacy and danger: The intricate nature of IBC, combined with its risks, may prevent several, particularly when simpler and less dangerous options are readily available.

Assigning around 10% of your regular monthly revenue to the policy is just not possible for most individuals. Utilizing life insurance policy as a financial investment and liquidity resource needs discipline and tracking of policy cash money worth. Seek advice from a financial consultant to figure out if boundless financial aligns with your priorities. Component of what you review below is just a reiteration of what has currently been said over.

So prior to you obtain right into a situation you're not gotten ready for, know the complying with initially: Although the idea is commonly marketed as such, you're not actually taking a loan from yourself. If that held true, you would not have to settle it. Rather, you're borrowing from the insurance policy business and need to repay it with rate of interest.

Some social networks posts advise using money value from whole life insurance policy to pay down bank card financial obligation. The idea is that when you pay back the financing with passion, the quantity will certainly be sent back to your financial investments. That's not just how it functions. When you repay the loan, a part of that rate of interest mosts likely to the insurance policy company.

For the initial several years, you'll be paying off the commission. This makes it exceptionally challenging for your policy to build up worth throughout this time around. Whole life insurance policy costs 5 to 15 times a lot more than term insurance. Many people simply can not manage it. So, unless you can pay for to pay a couple of to several hundred dollars for the following years or more, IBC won't function for you.

Royal Bank Infinite Avion Rewards

Not everyone must rely exclusively on themselves for monetary safety. If you call for life insurance policy, here are some valuable tips to think about: Think about term life insurance coverage. These plans give protection throughout years with substantial monetary responsibilities, like home loans, student loans, or when taking care of little ones. Ensure to look around for the best price.

Copyright (c) 2023, Intercom, Inc. () with Reserved Typeface Call "Montserrat". This Font style Software is certified under the SIL Open Typeface License, Version 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Reserved Font Style Call "Montserrat". This Font Software application is accredited under the SIL Open Up Font Style License, Variation 1.1.Miss to major content

Infinite Banking Forum

As a CPA focusing on actual estate investing, I have actually cleaned shoulders with the "Infinite Banking Concept" (IBC) more times than I can count. I have actually even interviewed experts on the topic. The primary draw, aside from the evident life insurance policy advantages, was constantly the concept of accumulating cash worth within an irreversible life insurance coverage plan and borrowing versus it.

Certain, that makes good sense. However honestly, I constantly believed that money would certainly be much better invested straight on financial investments as opposed to channeling it with a life insurance coverage policy Up until I found exactly how IBC can be integrated with an Irrevocable Life Insurance Policy Trust Fund (ILIT) to create generational wealth. Allow's begin with the essentials.

Cash Flow Banking Review

When you obtain versus your policy's cash money value, there's no set repayment routine, offering you the liberty to handle the car loan on your terms. On the other hand, the cash worth remains to expand based upon the policy's guarantees and dividends. This configuration enables you to gain access to liquidity without interrupting the long-term growth of your policy, supplied that the car loan and passion are handled sensibly.

The process continues with future generations. As grandchildren are born and expand up, the ILIT can acquire life insurance coverage plans on their lives. The depend on then builds up multiple plans, each with expanding money worths and fatality benefits. With these policies in position, the ILIT successfully comes to be a "Household Bank." Relative can take financings from the ILIT, making use of the money worth of the plans to fund investments, begin organizations, or cover significant costs.

An important element of handling this Household Financial institution is the use of the HEMS standard, which represents "Health, Education, Upkeep, or Assistance." This standard is commonly consisted of in trust arrangements to guide the trustee on just how they can disperse funds to recipients. By sticking to the HEMS standard, the trust guarantees that distributions are made for important needs and lasting support, safeguarding the trust's assets while still providing for member of the family.

Enhanced Versatility: Unlike inflexible small business loan, you manage the settlement terms when borrowing from your own policy. This allows you to framework settlements in such a way that lines up with your organization cash flow. bank on yourself scam. Improved Cash Money Flow: By financing company expenses via plan loans, you can potentially release up money that would or else be bound in standard finance settlements or tools leases

He has the same tools, but has actually also constructed added money value in his policy and received tax obligation advantages. And also, he now has $50,000 available in his policy to use for future opportunities or costs. Despite its possible advantages, some people continue to be cynical of the Infinite Financial Principle. Allow's resolve a couple of usual worries: "Isn't this just pricey life insurance policy?" While it's true that the premiums for a properly structured entire life policy might be more than term insurance coverage, it is very important to view it as greater than just life insurance policy.

Infinite Banking Concept Pros And Cons

It's concerning producing a versatile financing system that provides you control and offers several benefits. When made use of purposefully, it can match various other financial investments and service techniques. If you're interested by the capacity of the Infinite Financial Concept for your organization, right here are some actions to consider: Inform Yourself: Dive deeper into the concept via respectable publications, seminars, or appointments with knowledgeable professionals.

{kind=link}

Latest Posts

Bring Your Own Bank: Expanding The Ways Companies ...

Whole Life Insurance Bank On Yourself

Why You Should Consider Being Your Own Bank